Yesterday marked the launch of a new Policy Exchange report, Power 2.0, on how to build a smarter, greener, cheaper electricity system. The report argues that in order to further decarbonise the power system and integrate renewables, it is essential that we also create a smarter, more flexible power system to manage intermittent power supplies. Failure to do so could significantly increase the cost of decarbonising the power system and the economy more generally. Research by Imperial College shows that the system-wide benefits of creating a more flexible power system could be up to £8 billion per year by 2030 (or £90 per household per year).

The report was launched at an event yesterday, which included a keynote presentation from Sir David King (the former Chief Scientific Advisor, now Special Representative on Climate Change at the Foreign and Commonwealth Office) as well as representatives from Centrica, National Grid, and Open Energi. This blog summarises the key points from the report and event.

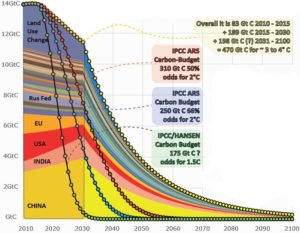

1 – Global decarbonisation plans are way off track

In his opening speech, Sir David outlined the scale of the challenge ahead if we are to mitigate climate change. Under the Paris Accord, global leaders have committed to limit global warming to less than 2oc above pre-industrial levels, and to make efforts to limit warming to 1.5oc. This is an enormous challenge, particularly given that global average temperatures have already increased by 1oc.

Countries have made a series of pledges to cut greenhouse emissions by around 15% by 2030 (referred to as “INDCs” or Intended Nationally Determined Contributions). The problem is that even if these pledges are delivered in full, this would put us on track for as much as 3oc of warming by the end of the century. In order to have a decent chance of limiting warming to 2oc or less, we will need to see far more rapid and deep cuts in global emissions. In fact, modelling suggests that limiting warming to 2oc or less (by 2100) will require global emissions to fall to ‘net zero’ during the second half of this century. It is hoped that countries will gradually ratchet up their carbon pledges in order to bridge this carbon gap – but at present this remains a hope. It will be interesting to see how this plays out in the COP22 meeting now underway.

Global INDCs compared with global carbon budgets (Source: Carbon Budget Accounting Tool)

2 – Need for targeted innovation to reduce the cost of clean energy

One of the barriers to countries tightening their carbon pledges is the likely costs associated with doing so. Whilst many individuals and nation states are concerned about climate change, there is a limit on how much people are willing to pay to do something about it (as discussed in a previous Policy Exchange report, The Customer is Always Right).

For this reason, it is imperative that industry and Governments work together to reduce the cost of low carbon technologies. To an extent this can be done through policy design – for example previous Policy Exchange reports have argued the case for competitive allocation of clean energy subsidies, as opposed to fixed Feed in Tariffs.

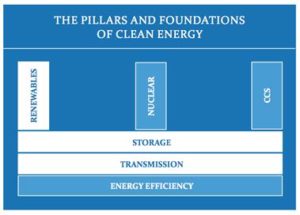

However, more significant reductions in the cost of clean technologies will likely be delivered through innovation. In his keynote speech, Sir David King described the ‘Mission Innovation’ initiative (previously called the ‘Global Apollo Programme’) which is aimed at boosting publically funded R&D into clean energy. 22 nations have already committed to double their spending on clean energy R&D to $30 billion per year by 2020, alongside significant investments by the private sector. The focus of the initiative is on renewables, storage and smart networks (on the basis that research into nuclear, CCS, and energy efficiency is already relatively well funded).

Global Apollo Programme Research Focus (Source: Sir David King / Global Apollo Programme)

3 – The power system in Great Britain is changing rapidly

Innovation will clearly play an important role going forwards, driving down the cost of low carbon technologies to accelerate their adoption. The Policy Exchange report highlights that the UK is already some way down the track towards a low carbon power system. The amount of renewables capacity on the system has increased ten-fold since 2000 (to 32.5GWs) whilst fossil fuel generation has and will continue to decline. Total power demand has reduced by some 15% since 2005, in part due to improvements in energy efficiency. Overall, the UK has achieved a 50% cut in power sector emissions since 1990. This is part of a broader transformation which has taken place since the privatisation of the power industry during the 1990s. The power system is becoming far more decentralised, with a decline of large-scale transmission-connected capacity and significant growth of small-scale ‘embedded’ generation and storage.

Evolution of the power system (Source: National Infrastructure Commission)

4 – New challenges for the power system

The trends towards decarbonisation and decentralisation are creating some significant challenges for the management and operation of the power system. The growth in intermittent renewables capacity adds to the challenge of balancing the power system on a second by second basis – since wind and solar output is dependent on the weather and more volatile than conventional sources of power. Meanwhile, the growth in decentralised capacity has led to some parts of the distribution grid becoming constrained, as there simply isn’t enough network capacity to get power away at peak times. This has led to a significant backlog of projects wishing to connect to the grid.

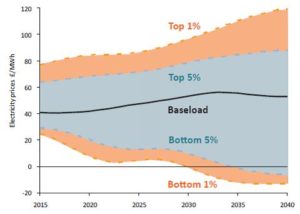

The power system has become much tighter in recent years, due to the loss of thermal capacity. This is already resulting in price spikes when there is a shortage of available capacity. At the launch of the Power 2.0 report, Jorge Pikunic (a Managing Director at Centrica) described how the frequency of price spikes is increasing. He suggested that power prices had exceeded £150/MWh on 12 occasions during the period 2010-15, but that there have been 25 similar price spikes during 2016 alone. During the course of the event itself, power prices in the Balancing Market surged to £2,500 per MWh on the back of low wind output and a number of plant outages. More generally, it is expected that the growth in renewables capacity will contribute to greater price volatility, increasing the frequency of price spikes and periods of negative pricing.

Spread of wholesale electricity prices (Source: Aurora Energy Research)

5 – Levelling the playing field

These challenges underline the need to build a more flexible power system. Increasing the amount of flexible capacity can result in economic and environmental benefits, by optimising the use of low carbon generation, reducing the need for fossil fuel backup capacity, and avoiding investment to reinforce the grid. Overall it is estimated that increasing the flexibility of the power system could lead to savings worth up to £8 billion per year by 2030.

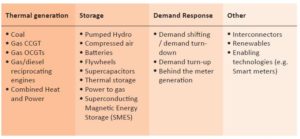

Many different technologies can provide this flexibility as follows:

However, it is clear that not all of these technologies are treated equally within the current set of policies and regulations. Specifically, the current rules and regulations appear to favour ‘dirty’ forms of flexibility such as diesel generators over ‘clean’ forms of flexibility such as battery storage or demand response.

One example of this is the issue of ‘double charging’. When power is consumed, a number of levies are charged relating to the cost of clean energy policies such as the Renewables Obligation and Feed in Tariffs. In the case of storage these charges are levied twice – once when the storage device is charged, and again when the same power flows to an end consumer. This presents a major cost to storage operators, which is not borne by other forms of flexibility such as thermal power stations, and puts storage at a commercial disadvantage.

At the other end of the spectrum, some developers are making very high financial returns from building diesel generators. Diesel generators produce significant quantities of greenhouse gasses emissions and local pollution, but are generally small enough to fall below the threshold of emissions regulations (such as the Large Combustion Plant Directive) and the EU Emissions Trading Scheme. The Policy Exchange report suggests tightening emissions regulations for small-scale generators, to limit the deployment of diesel. Diesel generators have also benefitted from a number of financial incentives, such as the ‘embedded benefits’ available for small-scale generators connected to the distribution grid, and tax breaks such as the Enterprise Investment Scheme.

The Policy Exchange report makes a number of recommendations on how to level the playing field between these technologies, through changes to policies and regulations.

6 – Need for reform of the wholesale market

Beyond this, there is a need for some longer-term thinking about how to reform the power market to value and encourage flexibility. The challenges identified above cannot be tackled purely through a piecemeal and incremental approach to policymaking. What is needed is a more substantial overhaul of the foundations of the power market, so that it performs as a well-functioning market. The Policy Exchange report suggests a substantial redesign of the wholesale market in order to increase its dynamism, efficiency and flexibility. It suggests moving to a system of “nodal pricing” – drawing on the example of power markets in New Zealand, Singapore, and the US.

At present we have a single power market in Britain, which neither reflects the geographical patterns of demand and supply, nor the physical constraints within the power network. Under nodal pricing, the market is made up of a number of trading nodes, with network constraints are hard-wired into the market. This means that the market price varies by location (as shown in the heat map below). Evidence from the PJM market in the US suggests that the use of nodal pricing has led to consumer savings worth $2.2 billion per year.

7 – Simplifying flexibility markets

Finally, the Policy Exchange report also suggests a radical simplification of ancillary markets. As shown below, there are a bewildering number of markets for flexibility within the GB power system – including price-based markets, together with many services procured by National Grid. This complexity creates a barrier to entry for firms wishing to provide flexibility, as well as overlaps between policies and unintended consequences.

The Policy Exchange report suggests that these markets should be consolidated and simplified, with much greater transparency, and regular, technology-neutral, competitive auctions. The report cites the example of Germany, where there are three main ancillary markets, procured via weekly auctions on a single web platform. Demand and supply bid in the same auctions (as opposed to GB where there are often separate incentives for demand response). Although it remains imperfect, the German model shows what can be done to simplify ancillary markets.

Overall, the Policy Exchange report has been well-received and has already provoked much discussion. In his closing remarks, Sir David King said that the report is ‘precisely what is needed to stimulate thinking’. The Government has already progressed its own thinking on how to build a smart power system, and is expected to issue a call for evidence on this issue ‘imminently.’