The Budget has two parts. First comes the forecasts, now produced by the independent OBR. These tell the Chancellor how much he has (or hasn’t got). The second part is what he chooses to do with what money there is. This blog examines the first of these issues.

It is important to review official forecasts as they are the basis for spending decisions today and planning for the future. Given this important role, they must be robust and, as was seen with the overly pessimistic Treasury forecasts regarding Brexit, they are not always right.

These forecasts come not directly from the Treasury but from the independent Office of Budget Responsibility (OBR). The OBR has been generally over-optimistic about the growth of GDP, and hence government revenues, since its foundation by George Osborne in 2010. As a result, its forecasts for the public sector’s deficit have been wide of the mark. A balanced budget was originally forecast for 2015, only to be put back in every successive year, until it is now expected, ten years later. Experience of previous inaccuracies has, perhaps, led to a forecast downgrade. The OBR used to forecast GDP growth at a steady 2.1% per annum, but now predicts growth at the slow rate of close to 1.4%per annum. If true, this slow rate of growth would give any Chancellor little headroom for give-aways.

My own modelling suggests that the new OBR forecasts are probably now a little pessimistic, but much depends on the details of Brexit. In the absence of any firmer guidance, the OBR takes the PM’s Florence speech as an indicator of what is likely to happen. Since the OBR forecasts only go as far as 2022 it has not needed to take a long-term view on what the eventual post-Brexit trade arrangements will be. However, by 2022 the Government’s intention is that the UK will be out of both the Single Market and Customs Union. It is not known, of course whether by then the UK will have a free-trade agreement with the EU27, or will instead have ‘no deal’ and hence fall back on World Trade Organisation rules. The OBR is not necessarily assuming a two year ‘implementation’ period from 2019-21 in which the UK remains inside the Single Market and Customs Union. Instead it merely assumes that migration will fall, and that growth in trade will slow.

What is noticeable is that the OBR predict a slight pick-up in economic growth in 2021 and 2022. No sign here of the Treasury’s long-term forecast of a major loss of GDP due to Brexit. We have argued elsewhere that the Treasury’s estimates for the long-term impact of Brexit are deeply flawed and thus approve of an OBR decision to ignore them. Although the Treasury’s Brexit forecasts are a dead-letter in government thinking, they still underpin the pessimism of many commentators, and it would be helpful if the OBR were more explicit on what it believes about the range of possibilities for the immediate post-Brexit years.

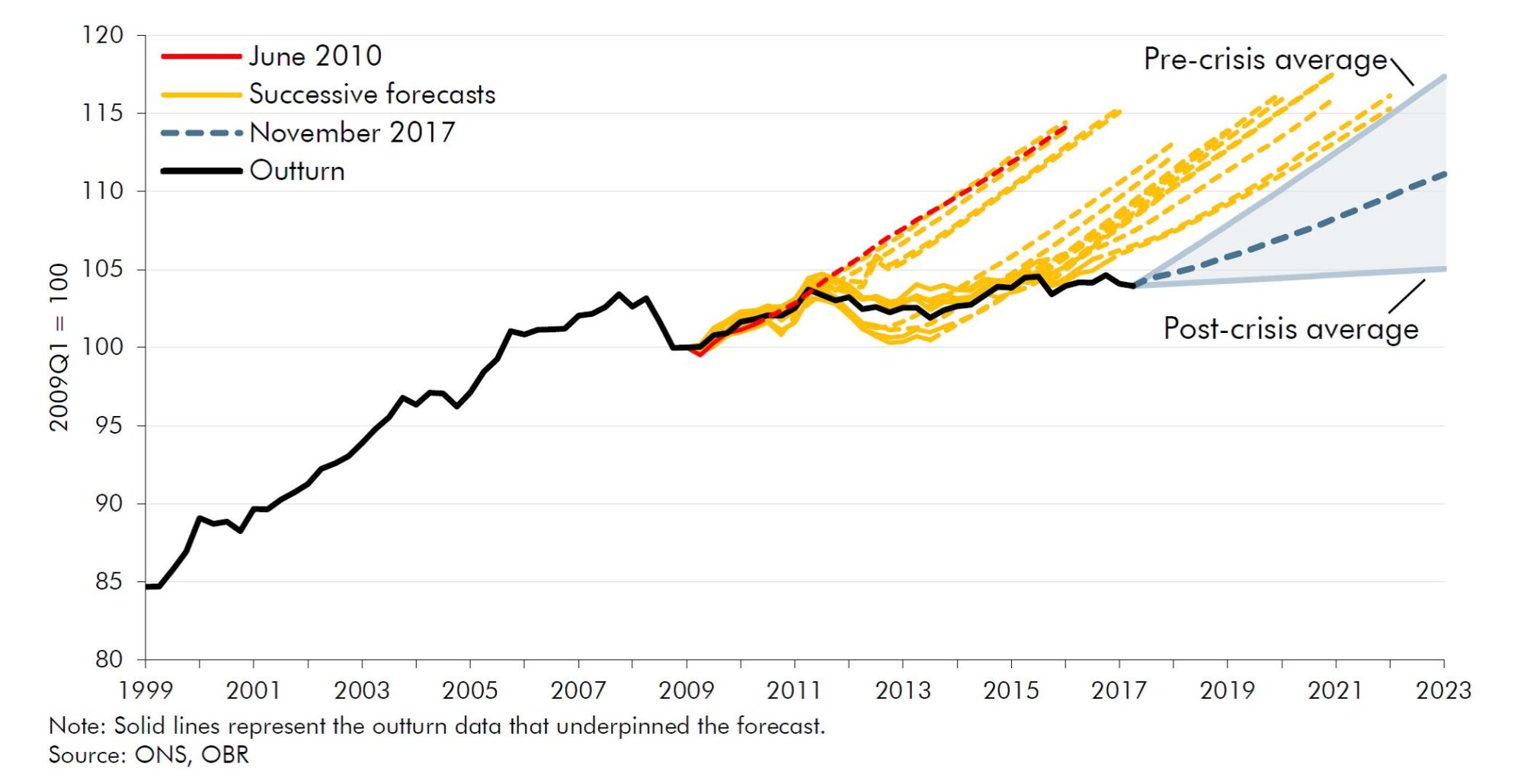

Since slow growth in the UK is the key constraint on what any responsible Chancellor can achieve, it is worth explaining why the OBR has been so far adrift in the past, and worth examining whether we can have much confidence in its new forecasts. The OBR forecasts for GDP are really assumptions, and somewhat arbitrary assumptions at that. These have tended to be treated in the media with unrealistic levels of reverence and have distorted public policy-making. What the OBR do is to make an assumption about the future path of labour productivity. In the past they have usually assumed a rapid return to pre-2009 rates of productivity growth at close to 2% per annum. Reality has continually disappointed, and the chart below shows the extent of OBR over-optimism on productivity. The OBR now assumes a growth rate of productivity close to 1% per annum, around half of the previous assumption. Together with other assumptions about the growth of population, employment rates and hours worked, the OBR generates its forecasts for GDP. Instead of casting these in budgetary stone, they should be treated as one possible scenario, so that we can be more realistic about the high degree of uncertainty in any fiscal prediction.

Productivity (output per hour) OBR Projections and Actual Outurns

Productivity (output per hour) OBR Projections and Actual Outurns

Like most economists, those in the OBR have little obvious understanding of why productivity growth has slowed, the so-called ‘productivity puzzle’. Instead the OBR just extrapolates from recent experience. While their current best guess seems to us to be reasonable, if a little pessimistic, it is important to develop a better understanding so that productivity can grow faster in future and the tight constraints on public spending can be relaxed. Our view, published elsewhere, is that the loss of manufacturing production to China and Eastern Europe has left the UK with an overwhelmingly service economy. The importance of this is that while productivity has traditionally grown at 3% per annum, output in services has grown at half that rate. A predominantly services economy puts a ceiling on UK productivity growth of close to 1.5%. An aging population and full employment additionally mean that annual growth rates in GDP are likely to be even slower than this.

This is not the whole story because productivity growth has slowed down since 2012 even within the UK’s residual manufacturing sector. It seems likely that production is now so automated that most manufacturing employees are in design, sales, management and other occupations not directly responsive to the level of production. UK manufacturing no longer has masses of production-line workers who can be laid off when sales are sluggish. Slow recent growth in manufacturing output has not thus led to staff layoffs, and productivity has hardly grown. To raise productivity in manufacturing, output will have to expand. The recent depreciation of sterling has helped a little, but larger improvements in competitiveness are needed. The current exchange rate of 1.3 dollars to the pound is still too high to compete with Chinese competitors, many of whom are automating rapidly. A further fall in sterling, which may accompany the UK’s exit from the single market, would be helpful. At this point it may be possible to begin a long process of re-industrialisation, moving labour from low productivity services (which may as a result increase their automation) and into higher productivity technical and managerial roles within new manufacturing activities. At the same time, rising interest rates are likely to weed out large numbers of low-productivity ‘zombie’ firms.

In Part 2 of our Budget analysis, we will examine how the Chancellor decided to use the money the forecast afforded him.